2026 Municipal Bond Opportunities: Tax-Exempt Income & High Yields

Advertisement

In the dynamic landscape of financial markets, investors are constantly seeking avenues that offer both stability and attractive returns. Among the myriad of investment options, 2026 municipal bonds stand out as a particularly compelling choice, especially for those looking to optimize their after-tax income. These bonds, issued by state and local governments to finance public projects, offer a unique combination of tax advantages and relatively secure income streams. As we approach the mid-2020s, understanding the nuances and opportunities presented by 2026 municipal bonds becomes paramount for savvy investors.

The allure of municipal bonds primarily stems from their tax-exempt status. For many investors, the income generated from these bonds is exempt from federal income tax, and often from state and local taxes if the bondholder resides in the issuing state. This tax advantage can significantly boost the effective yield, making municipal bonds an attractive alternative to other taxable fixed-income investments. With an eye towards 2026, the specific maturity date adds a layer of predictability and planning for investors with short to medium-term financial goals.

This comprehensive guide delves deep into the world of 2026 municipal bonds, exploring their benefits, market dynamics, and strategic considerations for investors. We will uncover why these instruments are gaining traction, how to identify promising opportunities, and what factors to consider when integrating them into your investment portfolio. Whether you are a seasoned investor or new to fixed income, understanding 2026 municipal bonds can unlock a powerful tool for wealth preservation and growth.

Advertisement

Understanding 2026 Municipal Bonds: A Foundation for Investment

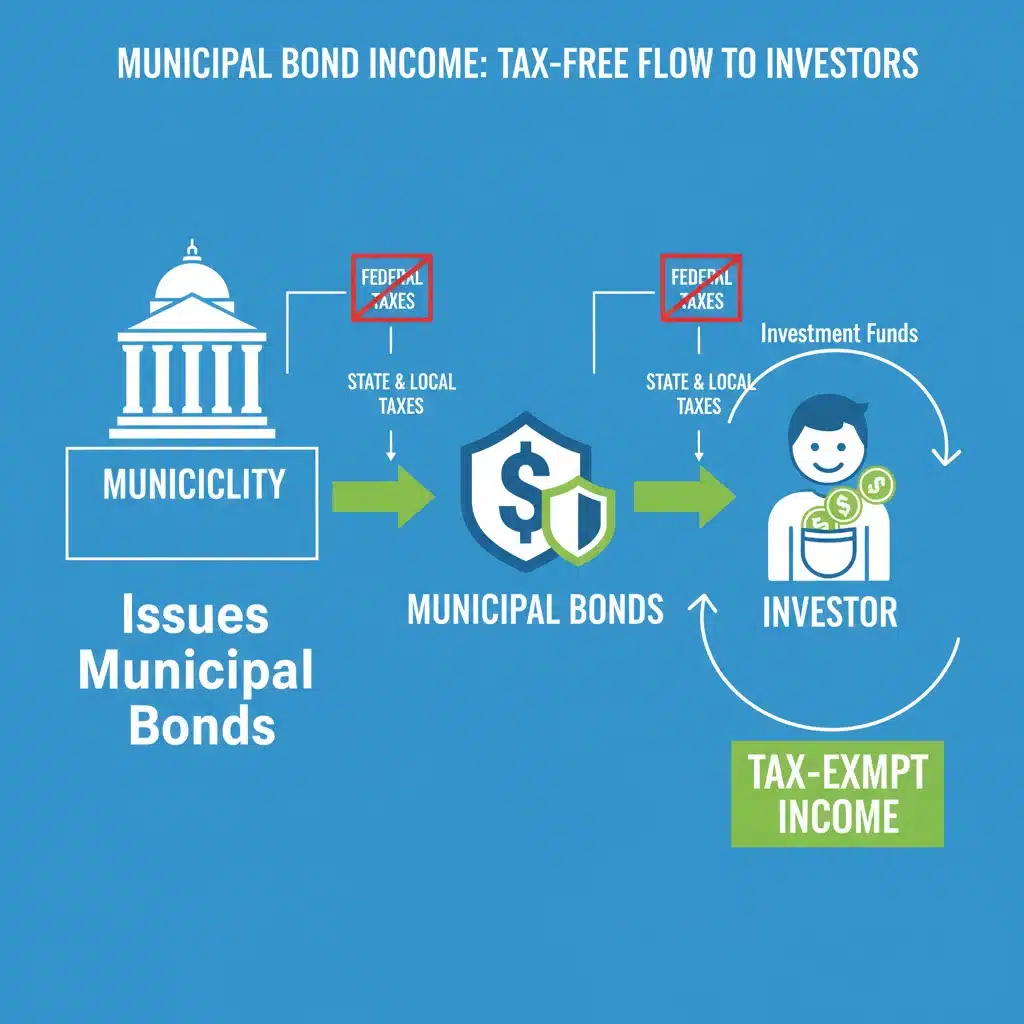

At its core, a municipal bond is a debt security issued by a state, municipality, or county to finance its capital expenditures, such as building schools, hospitals, highways, or sewer systems. When you purchase a municipal bond, you are essentially lending money to a local government entity. In return, the issuer promises to pay you periodic interest payments (usually semi-annually) and to repay the principal amount on a specified maturity date. In the context of 2026 municipal bonds, this maturity date is set for the year 2026, offering a clear timeline for your investment.

The Appeal of Tax-Exempt Income

The most significant advantage of municipal bonds, and a primary driver for investors considering 2026 municipal bonds, is their tax-exempt status. Interest earned on these bonds is typically exempt from federal income tax. Furthermore, if you purchase a bond issued by a municipality within your home state, the interest may also be exempt from state and local income taxes. This “triple tax exemption” can be a substantial benefit, particularly for investors in higher tax brackets. To truly appreciate this, one must compare the tax-equivalent yield of a municipal bond to that of a taxable bond. For instance, a 3.2% tax-exempt yield on a municipal bond could be equivalent to a much higher taxable yield, depending on your marginal tax rate.

Types of Municipal Bonds

While all municipal bonds share the common characteristic of being issued by government entities, they come in different forms, each with its own security features:

Advertisement

- General Obligation (GO) Bonds: These bonds are backed by the full faith and credit of the issuing municipality, meaning the issuer pledges its taxing power to repay the debt. They are generally considered very safe due to the issuer’s ability to raise taxes to meet its obligations.

- Revenue Bonds: These bonds are repaid from the revenue generated by a specific project, such as tolls from a highway, user fees from a water system, or lease payments from a public facility. Their creditworthiness depends on the success and revenue-generating capacity of the project they finance.

- Special Assessment Bonds: These are repaid from assessments levied on properties that benefit from a specific project, like a new sidewalk or street light.

When looking at 2026 municipal bonds, it’s crucial to understand which type of bond you are investing in, as it directly impacts the risk profile and the source of repayment.

Why Focus on 2026 Municipal Bond Opportunities?

The year 2026 is approaching, and bonds maturing in this timeframe offer specific advantages for investors. A mid-term maturity, like 2026, provides a balance between short-term liquidity and long-term yield potential. Investors who have a defined financial goal around 2026, or who are looking to ladder their bond portfolio, will find these bonds particularly appealing.

Predictability and Planning

For individuals planning for specific expenses or looking to re-evaluate their investment strategy in a few years, 2026 municipal bonds offer a clear exit point. This predictability allows for better financial planning, whether it’s for a down payment on a house, college tuition, or a significant retirement milestone. Knowing the exact maturity date helps in managing cash flow and re-investing capital.

Current Market Conditions and Yields

The current interest rate environment plays a significant role in the attractiveness of municipal bonds. While interest rates fluctuate, periods of higher rates can make new bond issues, including 2026 municipal bonds, offer more competitive yields. A reported 3.2% yield, if tax-exempt, can be highly competitive when compared to taxable alternatives, especially after considering inflation and the purchasing power of your investment.

Key Benefits of Investing in 2026 Municipal Bonds

Beyond the fundamental tax advantages and maturity-specific planning, 2026 municipal bonds offer several other compelling benefits that make them a cornerstone of many diversified investment portfolios.

1. Tax-Exempt Income: Maximizing After-Tax Returns

As previously highlighted, the tax-exempt nature of municipal bond interest is perhaps their most celebrated feature. For high-net-worth individuals and those in higher tax brackets, the ability to earn income free from federal, and often state and local, taxes can significantly enhance net returns. This is not merely a small saving; it can translate into a substantial increase in your effective yield. Consider the scenario where a taxable bond yields 5%. For an investor in the 30% federal tax bracket, the after-tax yield drops to 3.5%. If a 2026 municipal bond offers a 3.2% tax-exempt yield, it is nearly as good as the 5% taxable bond, and potentially better if state and local taxes are also avoided. This comparison underscores the power of tax-exempt income.

2. Relatively Low Risk

Municipal bonds are generally considered one of the safer investment options, especially when compared to equities or corporate bonds. The default rate for municipal bonds has historically been very low, significantly lower than that of corporate bonds. This stability is largely due to the taxing power of government entities (for GO bonds) and the essential nature of the projects they fund (for revenue bonds). While no investment is entirely risk-free, the robust backing and public utility of municipal projects contribute to their high credit quality. When evaluating 2026 municipal bonds, paying attention to credit ratings from agencies like Moody’s, S&P, and Fitch is crucial for assessing specific bond safety.

3. Diversification Benefits

Adding 2026 municipal bonds to a portfolio can provide valuable diversification. Their performance is often less correlated with other asset classes, such as stocks, which can help reduce overall portfolio volatility. During periods of market uncertainty or economic downturns, municipal bonds often serve as a safe haven, preserving capital and generating steady income when other investments may be struggling. This counter-cyclical characteristic makes them an excellent tool for risk management.

4. Consistent Income Stream

For investors seeking predictable income, municipal bonds are ideal. They typically pay interest semi-annually, providing a steady cash flow that can be used for living expenses, reinvestment, or other financial goals. The fixed nature of these payments makes financial planning much simpler and more reliable, a key advantage for retirees or those dependent on investment income.

Navigating the Market for 2026 Municipal Bonds

While the benefits are clear, successfully investing in 2026 municipal bonds requires a strategic approach to market navigation. Understanding how to research, select, and manage these investments is crucial for maximizing their potential.

Researching Issuers and Credit Quality

Before investing in any municipal bond, thorough research into the issuer’s financial health is paramount. For 2026 municipal bonds, this means examining the fiscal stability of the state or local government, its debt burden, economic outlook, and demographic trends. Credit ratings from independent agencies provide an invaluable snapshot of an issuer’s ability to repay its debt. Higher-rated bonds (e.g., AAA, AA) generally carry lower risk but may offer slightly lower yields, while lower-rated bonds (e.g., BBB) might offer higher yields to compensate for increased risk. It’s essential to strike a balance that aligns with your risk tolerance.

Understanding Yields and Pricing

Bond prices and yields move inversely. When interest rates rise, existing bond prices fall, and new bonds are issued with higher yields. Conversely, when interest rates fall, existing bond prices rise, and new bonds offer lower yields. For 2026 municipal bonds, current market interest rates will significantly influence the yield you can expect. A 3.2% yield is a strong indicator of current market conditions, but it’s important to understand how this yield compares to historical averages and other investment opportunities. Always consider the “yield to maturity,” which factors in the bond’s current market price, coupon rate, and time to maturity.

Callable Bonds and Reinvestment Risk

Some municipal bonds are callable, meaning the issuer has the option to redeem the bond before its stated maturity date. This often happens if interest rates fall, allowing the issuer to refinance its debt at a lower cost. While a callable 2026 municipal bond could mature earlier than expected, it typically offers a higher yield to compensate for this risk. Investors should be aware of call provisions and understand the potential for reinvestment risk—the risk that if a bond is called, you may have to reinvest the proceeds at a lower interest rate.

Strategic Investment Approaches for 2026 Municipal Bonds

To effectively leverage 2026 municipal bonds, investors can employ several strategic approaches tailored to their financial goals and risk profiles.

Bond Laddering

Bond laddering is a popular strategy where an investor buys a series of bonds with staggered maturity dates. For example, you might buy bonds maturing in 2024, 2025, 2026, 2027, and so on. As each bond matures, the principal can be reinvested in a new bond with the longest maturity in the ladder. This strategy helps mitigate interest rate risk, provides regular income, and ensures that a portion of your portfolio is regularly liquid. Incorporating 2026 municipal bonds into a ladder can provide a consistent stream of tax-exempt income while allowing for periodic adjustments to your portfolio based on prevailing interest rates.

Targeting Specific Financial Goals

If you have a specific financial goal set for 2026, such as funding a child’s education or making a significant purchase, investing in 2026 municipal bonds can be a highly effective strategy. By matching the bond’s maturity date with your financial objective, you can ensure that the principal will be available exactly when you need it, with the added benefit of tax-exempt income along the way. This approach minimizes market timing risk for that specific goal.

Geographic Diversification

While investing in bonds from your home state offers the potential for triple tax exemption, it’s also wise to consider geographic diversification. Spreading your investments across different states and municipalities can reduce concentration risk. If one region faces economic challenges, your entire portfolio won’t be unduly affected. When diversifying, remember to calculate the after-tax yield for out-of-state bonds, as they may only be federally tax-exempt, not state or local. However, a strong out-of-state issuer might still offer a compelling after-tax yield compared to a weaker in-state issuer.

Risks Associated with 2026 Municipal Bonds

While generally considered safe, municipal bonds are not without risks. Understanding these risks is crucial for making informed investment decisions.

Interest Rate Risk

This is the risk that changes in prevailing interest rates will affect the value of your bond. If interest rates rise after you’ve purchased a 2026 municipal bond, the market value of your bond will likely fall. This is because new bonds will be issued with higher coupon rates, making your lower-coupon bond less attractive. However, if you hold the bond until maturity, you will still receive your principal back, regardless of interim price fluctuations.

Credit Risk

Although rare, there is a risk that the issuing municipality could default on its payments. This risk is higher for revenue bonds tied to specific projects that might underperform. Careful due diligence, including reviewing credit ratings and financial statements of the issuer, can help mitigate this risk. While 2026 municipal bonds are generally stable, a severe economic downturn or mismanagement could theoretically impact even highly rated issuers.

Inflation Risk

Inflation risk refers to the possibility that the purchasing power of your bond’s future interest payments and principal repayment will be eroded by inflation. If inflation rates are higher than your bond’s yield, your real return (after accounting for inflation) will be negative. This is a common risk for all fixed-income investments, and it’s why a diversified portfolio often includes assets that perform well in inflationary environments.

Liquidity Risk

Some municipal bonds, particularly those from smaller issuers or less common types, may not trade frequently, leading to liquidity risk. This means you might find it difficult to sell your bond quickly at a fair market price before its maturity date. For 2026 municipal bonds, this is typically less of a concern for widely traded issues but something to be aware of if considering niche offerings.

How to Invest in 2026 Municipal Bonds

Investing in 2026 municipal bonds can be done through several channels, each offering different levels of convenience and control.

Individual Bonds

You can purchase individual municipal bonds through a brokerage account. This approach allows you to select specific bonds that meet your criteria for maturity, credit quality, and state of issuance. It requires more research and active management but offers precise control over your investments. For those targeting 2026 municipal bonds, buying individual bonds ensures you lock in that specific maturity date.

Municipal Bond Funds (ETFs and Mutual Funds)

For investors who prefer a more diversified and professionally managed approach, municipal bond funds (both exchange-traded funds or ETFs and mutual funds) are an excellent option. These funds hold a portfolio of many different municipal bonds, providing instant diversification across various issuers, maturities, and geographies. While funds offer convenience, it’s important to remember that their net asset value (NAV) fluctuates, and they do not have a fixed maturity date like individual bonds. However, there are target-date municipal bond funds that mature in a specific year, such as 2026, which can mimic the characteristics of individual bonds.

Working with a Financial Advisor

A qualified financial advisor can provide invaluable guidance when investing in 2026 municipal bonds. They can help you assess your financial goals, risk tolerance, and tax situation to recommend suitable bonds or funds. An advisor can also assist with researching issuers, monitoring market conditions, and integrating municipal bonds into a broader investment strategy.

The Future Outlook for Municipal Bonds Towards 2026 and Beyond

As we look towards 2026, the municipal bond market is likely to remain a vital component of the fixed-income landscape. Several factors will continue to influence its appeal:

Infrastructure Spending

Governments at all levels continue to face significant infrastructure needs, from repairing aging roads and bridges to investing in new technologies and sustainable energy projects. This ongoing demand for funding ensures a steady supply of new municipal bond issues, including those maturing in 2026, providing ample opportunities for investors.

Interest Rate Environment

The trajectory of interest rates will always be a key determinant of municipal bond attractiveness. While predicting future rate movements is challenging, investors should remain informed about Federal Reserve policy and global economic trends. A rising rate environment might lead to higher yields on new issues, making 2026 municipal bonds even more appealing for those looking to lock in competitive returns.

Tax Policy Changes

While the tax-exempt status of municipal bonds has been a cornerstone of the U.S. tax code for decades, potential changes in tax policy could impact their relative attractiveness. Investors should stay abreast of legislative developments that might affect federal, state, or local tax rates, as these could alter the after-tax yield comparison with taxable investments.

Conclusion: Seizing the Opportunity with 2026 Municipal Bonds

2026 municipal bonds present a compelling investment opportunity for a wide range of investors. Their potent combination of tax-exempt income, relative safety, and predictable maturity makes them an excellent tool for diversification, income generation, and goal-oriented financial planning. With a reported yield of 3.2% (tax-exempt), these bonds offer a significant advantage over many taxable alternatives, especially for those in higher tax brackets.

By understanding the different types of municipal bonds, conducting thorough research on issuers, and employing strategic approaches like bond laddering, investors can effectively navigate the market. While risks such as interest rate fluctuations and credit risk exist, they can be managed through diversification and careful selection. As 2026 approaches, the opportunity to lock in attractive, tax-advantaged income streams through these essential public finance instruments is one that discerning investors should seriously consider.

Ultimately, incorporating 2026 municipal bonds into your portfolio can contribute to a more stable, tax-efficient, and diversified investment strategy, helping you achieve your financial objectives with greater confidence. Consult with a financial professional to determine how these bonds can best fit into your individual financial plan.