2026 Medicare Part B Premium Hike: Implications for Your Benefits and Budget

Advertisement

The 2026 Medicare Part B Premium Hike: What It Means for Your Benefits and Budget

As we navigate the ever-evolving landscape of healthcare, understanding future changes to vital programs like Medicare is paramount. For millions of Americans, Medicare Part B is a cornerstone of their health coverage, covering medically necessary services and preventive care. However, discussions and projections often point towards a potential Medicare Part B 2026 premium hike. This anticipated increase can have significant implications for beneficiaries’ budgets and access to care. This comprehensive guide will delve deep into what a potential 2026 Medicare Part B premium increase could mean for you, offering insights into its causes, effects, and actionable strategies for preparation.

The prospect of rising healthcare costs is a perennial concern, and Medicare premiums are no exception. For seniors and individuals with disabilities who rely on Medicare Part B, any adjustment to premiums directly impacts their disposable income and financial stability. Preparing for these changes well in advance is not just prudent; it’s essential for maintaining peace of mind and ensuring uninterrupted access to necessary medical services. Let’s explore the factors driving these potential changes and how you can proactively plan for them.

Understanding Medicare Part B: The Foundation of Your Coverage

Before we dissect the potential Medicare Part B 2026 premium hike, it’s crucial to have a solid understanding of what Medicare Part B entails. Medicare Part B is a component of Original Medicare, which also includes Part A (hospital insurance). While Part A primarily covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care, Part B covers a broad range of outpatient medical services.

Advertisement

What Does Medicare Part B Cover?

Medicare Part B is designed to cover medically necessary services and preventive services. This includes, but is not limited to:

- Doctor’s Services: Visits to your primary care physician and specialists.

- Outpatient Care: Services received in a hospital outpatient department, such as emergency room visits (that don’t result in an inpatient admission) and observation stays.

- Preventive Services: Screenings, vaccines, and certain wellness visits aimed at preventing illness or detecting it early.

- Medical Equipment: Durable medical equipment (DME) like wheelchairs, walkers, and oxygen equipment.

- Ambulance Services: Emergency transportation when other transportation could endanger your health.

- Mental Health Services: Outpatient mental health care, including therapy and counseling.

- Laboratory Tests and X-rays: Diagnostic services.

- Some Home Health Services: If prescribed by a doctor and you meet certain conditions.

For most beneficiaries, the monthly premium for Medicare Part B is deducted directly from their Social Security, Railroad Retirement Board, or Office of Personnel Management benefits. If you don’t receive these benefits, you’ll be billed directly.

The Mechanics of Medicare Part B Premiums and the IRMAA

The standard monthly premium for Medicare Part B is determined annually by the Centers for Medicare & Medicaid Services (CMS). However, not everyone pays the standard premium. A significant factor influencing what individuals pay is the Income-Related Monthly Adjustment Amount (IRMAA).

Advertisement

What is IRMAA?

IRMAA is an additional amount that some individuals pay on top of their Part B (and Part D) premiums if their modified adjusted gross income (MAGI) exceeds certain thresholds. These thresholds are adjusted annually, and the income used to determine your IRMAA for a given year is typically from two years prior. For example, your 2026 IRMAA will likely be based on your 2024 income. This means that if your income increased significantly in 2024, you could see a higher Part B premium in 2026, even before any general premium hike.

The IRMAA structure is progressive, meaning the higher your income, the higher your Part B premium. This mechanism is designed to ensure that those with higher incomes contribute more to the Medicare program.

Why a Medicare Part B 2026 Premium Hike is Anticipated

Several factors typically contribute to the annual adjustments in Medicare Part B premiums, and these same factors are likely to drive any potential hike in 2026. Understanding these drivers is key to comprehending the financial landscape of Medicare.

Rising Healthcare Utilization and Costs

One of the primary drivers of premium increases is the overall rise in healthcare costs. This includes:

- Increased Use of Medical Services: As the population ages, there’s a natural increase in the demand for medical services, including doctor visits, diagnostic tests, and treatments.

- Advancements in Medical Technology: New drugs, advanced medical devices, and innovative treatments often come with higher price tags, driving up the cost of care.

- Inflation in Healthcare: Like other sectors of the economy, the healthcare industry experiences inflation, leading to higher prices for services, supplies, and labor.

Prescription Drug Costs

While Medicare Part D covers most prescription drugs, the cost of certain drugs administered in an outpatient setting (e.g., infusions in a doctor’s office) falls under Part B. The escalating prices of these specialty drugs can significantly impact Part B expenditures.

Medicare Trust Fund Solvency

Medicare Part B is funded through a combination of beneficiary premiums and general revenue from the federal government. The financial health of the Supplementary Medical Insurance (SMI) Trust Fund, which pays for Part B, is regularly assessed. If projections show a need for more revenue to cover anticipated expenditures, premium increases are often considered to maintain the fund’s solvency.

Impact of Economic Factors

Broader economic conditions, such as inflation rates and the overall economic growth, can also play a role. High inflation can increase the cost of providing healthcare services, indirectly pushing up premiums.

The Potential Impact of a Medicare Part B 2026 Premium Hike on Your Budget

A premium hike, regardless of its size, can have a tangible effect on the financial well-being of Medicare beneficiaries. For those living on fixed incomes, even a modest increase can necessitate adjustments to their monthly budget.

Reduced Disposable Income

The most immediate effect of a premium increase is a reduction in disposable income. For retirees who often rely on Social Security benefits as their primary income source, a higher Part B premium means less money available for other essential expenses like food, housing, utilities, and leisure activities.

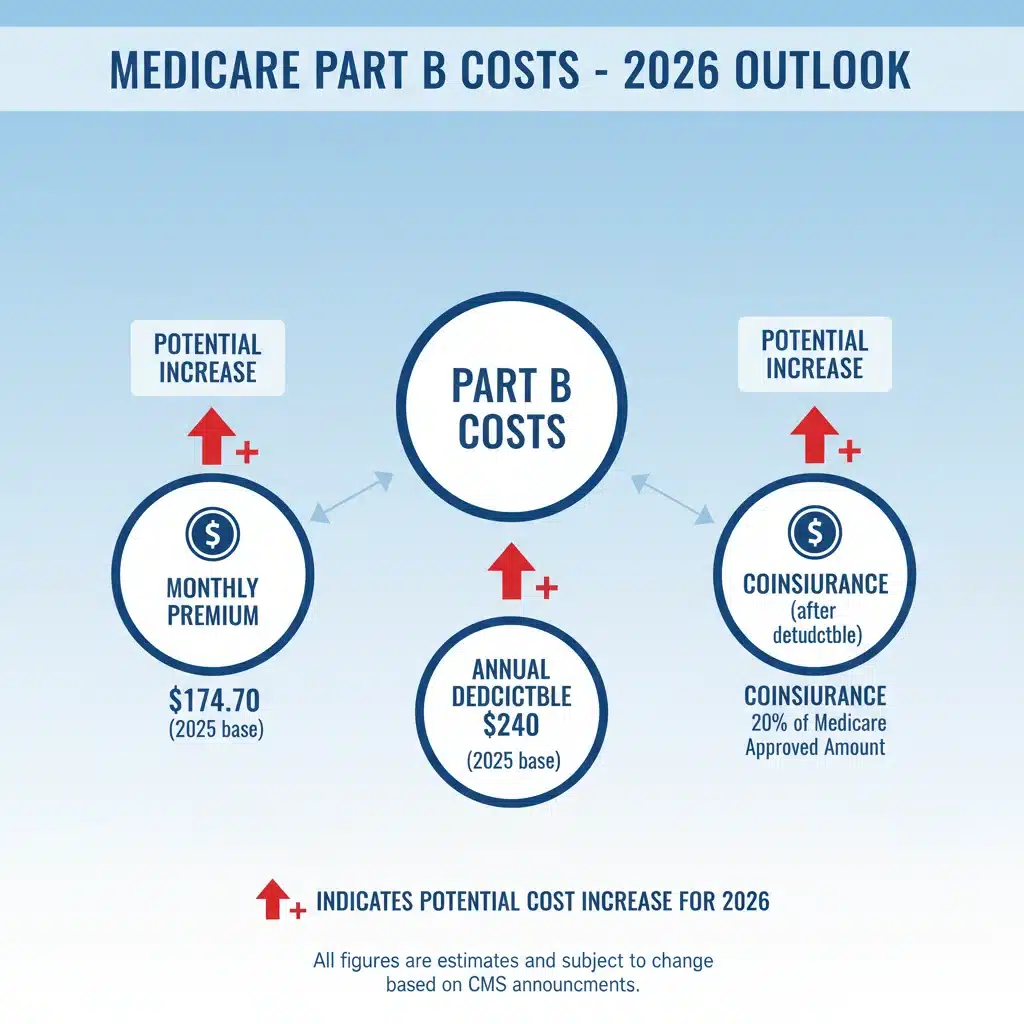

Increased Out-of-Pocket Costs

It’s important to remember that the Part B premium is just one component of your total healthcare costs. You also have a deductible, and after meeting the deductible, you typically pay 20% of the Medicare-approved amount for most doctor services and durable medical equipment. If the overall cost of healthcare increases, even if your coinsurance percentage remains the same, the actual dollar amount you pay out-of-pocket can rise.

Impact on Low-Income Beneficiaries

While Medicare offers programs like the Medicare Savings Programs (MSPs) to help low-income individuals with their Part B premiums, a general increase can still strain their already tight budgets, especially for those who just miss the eligibility cutoffs for assistance.

Planning for Future Healthcare Expenses

The consistent upward trend in healthcare costs, including Part B premiums, underscores the critical need for robust financial planning in retirement. Many financial advisors recommend allocating a significant portion of retirement savings specifically for healthcare expenses, recognizing that these costs will likely continue to grow.

Strategies to Prepare for the Medicare Part B 2026 Premium Hike

While the exact figures for the 2026 Medicare Part B premium hike are still speculative, proactive planning can help mitigate its impact. Here are several strategies to consider:

1. Review Your Budget and Financial Plan

Now is an excellent time to re-evaluate your monthly budget. Identify areas where you might be able to cut back or reallocate funds to accommodate a higher Part B premium. If you have a financial advisor, schedule a meeting to discuss how potential Medicare changes fit into your overall retirement plan.

2. Optimize Your Healthcare Coverage

Consider whether your current Medicare coverage is still the best fit for your needs and budget. Options include:

- Medicare Advantage (Part C): These plans are offered by private companies approved by Medicare and cover all Part A and Part B services. Many Medicare Advantage plans also include prescription drug coverage (Part D) and extra benefits like vision, dental, and hearing. Some plans may have lower or even $0 monthly premiums, but you still pay your Part B premium.

- Medigap (Medicare Supplement Insurance): Medigap policies help pay some of the out-of-pocket costs that Original Medicare doesn’t cover, such as deductibles, copayments, and coinsurance. While Medigap policies have their own premiums, they can provide more predictable out-of-pocket expenses, which might be beneficial if Part B costs rise.

Annually, during the Open Enrollment Period (October 15 to December 7), you have the opportunity to make changes to your Medicare coverage. Use this time wisely to compare plans and ensure you have the most cost-effective and comprehensive coverage.

3. Understand and Manage Your IRMAA

Since IRMAA is based on your income from two years prior, there might be opportunities to manage your income to potentially reduce your IRMAA in future years. This could involve strategies like:

- Tax-Efficient Withdrawals: If you have both pre-tax (e.g., traditional IRA, 401(k)) and post-tax (e.g., Roth IRA, taxable brokerage accounts) retirement savings, consider strategies for withdrawing from these accounts in a way that minimizes your MAGI.

- Qualified Charitable Distributions (QCDs): If you are over 70½ and take Required Minimum Distributions (RMDs) from your IRA, making a QCD directly from your IRA to a charity can reduce your taxable income and thus your MAGI.

- Timing of Capital Gains: If you sell investments, be mindful of how capital gains will impact your MAGI.

Consult with a tax advisor or financial planner to explore IRMAA-reducing strategies that are appropriate for your specific financial situation.

4. Explore Medicare Savings Programs (MSPs)

If you have limited income and resources, you might qualify for one of the Medicare Savings Programs (MSPs). These programs can help pay for your Part B premiums, deductibles, and coinsurance. There are different types of MSPs, each with varying income and resource limits. Even a small amount of assistance can make a significant difference.

5. Stay Informed

Keep abreast of official announcements from CMS and the Social Security Administration regarding Medicare Part B premiums. These announcements typically occur in the fall of the preceding year (e.g., fall 2025 for 2026 premiums). Reliable sources include Medicare.gov, the Social Security Administration website, and reputable financial news outlets.

The Broader Implications: Healthcare Affordability and Policy

The discussion around the Medicare Part B 2026 premium hike is part of a larger national conversation about healthcare affordability, the sustainability of entitlement programs, and the economic well-being of seniors. Policymakers continuously grapple with balancing the need to provide comprehensive healthcare benefits with the imperative to control costs and ensure the long-term solvency of Medicare.

The Role of Legislation

Legislative actions can also influence Medicare Part B premiums. Congress may pass laws that affect drug pricing, healthcare provider reimbursement rates, or the funding mechanisms for Medicare, all of which can have ripple effects on premiums. For example, recent legislation aimed at allowing Medicare to negotiate drug prices could, in the long term, help moderate some Part B costs for certain medications.

Preventive Care and Wellness

While not a direct solution to premium hikes, focusing on preventive care and maintaining a healthy lifestyle can indirectly help manage overall healthcare costs. By staying healthy, beneficiaries may reduce their need for extensive medical interventions, thereby potentially lowering their out-of-pocket expenses for deductibles and coinsurance, even if premiums rise.

Real-World Scenarios: How a Hike Could Play Out

Let’s consider a few hypothetical scenarios to illustrate the potential impact of a Medicare Part B 2026 premium hike:

Scenario 1: Standard Premium Increase

Imagine the standard Part B premium increases by $10-$15 per month. For a beneficiary on a fixed income of $2,000 per month, this represents a significant proportional increase in their healthcare outlay. This person might need to cut back on discretionary spending or find ways to reduce other fixed costs.

Scenario 2: IRMAA Threshold Adjustment

If the IRMAA income thresholds are not significantly adjusted for inflation, more people could find themselves falling into higher IRMAA brackets, even if their real income hasn’t increased dramatically. This could lead to a substantial jump in their Part B premium, potentially by hundreds of dollars per month for those at the cusp of a new bracket.

Scenario 3: Combined Effects

The most challenging scenario involves both a standard premium increase and an IRMAA adjustment. A beneficiary who experiences both could see a considerable portion of their Social Security cost-of-living adjustment (COLA) absorbed by the increased Part B premium, leaving little net gain in their monthly income.

These scenarios highlight why it’s so important to not only be aware of the potential hike but also to understand your individual financial situation and how it interacts with Medicare’s premium structure.

The Importance of Staying Proactive and Informed

The future of Medicare Part B premiums, particularly for 2026, remains a subject of ongoing analysis and projection. While definitive numbers are yet to be released, the historical trends and current economic climate suggest that beneficiaries should prepare for potential increases. Being proactive means not waiting until the official announcement but rather taking steps now to review your financial situation, understand your coverage options, and explore avenues for assistance if needed.

Engaging with trusted resources such as Medicare.gov, your State Health Insurance Assistance Program (SHIP), or a qualified financial advisor can provide personalized guidance. These resources can help you navigate the complexities of Medicare, understand the nuances of premium adjustments like IRMAA, and make informed decisions about your healthcare coverage.

Remember, Medicare is a dynamic program, and its costs are subject to change. By staying informed and planning ahead, you can better manage the financial impact of a Medicare Part B 2026 premium hike and ensure that your healthcare needs continue to be met without undue financial strain. Your health and financial security are too important to leave to chance; empower yourself with knowledge and proactive planning.

Conclusion: Navigating the Future of Medicare Part B

The anticipated Medicare Part B 2026 premium hike is a significant consideration for current and future beneficiaries. Driven by a confluence of factors including rising healthcare costs, increased utilization, and the need to maintain the solvency of the Medicare trust fund, these premium adjustments are a regular feature of the Medicare landscape. While the exact figures will only be announced closer to the end of 2025, the prudent approach is to begin preparing now.

By understanding what Medicare Part B covers, how premiums are determined (including the impact of IRMAA), and the various strategies available for mitigation, beneficiaries can empower themselves to navigate these changes effectively. Reviewing your budget, optimizing your healthcare coverage, exploring Medicare Savings Programs, and seeking professional financial advice are all crucial steps in this preparation. The goal is to ensure that any premium increase does not unduly compromise your access to essential medical care or your overall financial stability in retirement.

Staying informed through official channels and engaging in thoughtful financial planning will be your best defense against the uncertainties of future healthcare costs. Medicare is an invaluable program, and with careful planning, you can continue to leverage its benefits to support your health and well-being for years to come.